Trump Accounts

New Option for Creating Family Wealth

With the passage of HR 1 (otherwise known as the One Big Beautiful Bill), there will soon (on July 4, 2026) be a new way to help your children and grandchildren save money. With the recently released temporary regulations on how these accounts will work, we can start to determine if they are a good option for you. But first, let’s look at the other ways that you can help your children save:

1) An old fashioned bank account or taxable investment account.

Pros - Easy to set up and no restrictions on investment options. Money can be taken out for any purpose and any time.

Cons - Taxable and subject to Kiddie Tax if investment income exceeds $2,700 (2026 limit). That means if the child’s investment income is over $2,700, it will be taxed at the parent’s rate rather than the child’s lower rate.

Best For - Teaching children to save and manage their allowance and high school job earnings.

2) ROTH IRA account.

Pros - The money grows tax free. Your child’s retirement savings start before they can walk gives and gives them the power of long term investing. Investment options are nearly limitless.

Cons - To contribute the child must have earned income equal to the amount contributed to the ROTH. For 2026, the ROTH IRA contribution limit is only $7,500. Tax for non-approved distributions.

Best For - A business owner who can employee a young child for modeling and wants to start the child off on stable financial footing. The ROTH IRA contributions can always be withdrawn tax-free but earnings are taxable before 59.5 unless they are used for a long list of exemptions (like higher education costs and first time home purchase).

3) The 529 Plan.

Pros - No annual contribution limits and lifetime limits in the six figures (varies by state). While no Federal deduction, 30 states have tax credits for contributions. The funds grow tax-free and withdrawals are tax-free if used for qualified education costs. If the child does not use the entire balance for education, the funds can be transferred to other family members or $35,000 can be converted over to a ROTH IRA.

Cons - Depending upon the plan, the investment options can be limited. The 529 must be opened 15 years prior to the ROTH conversion.

Best For - Anybody that wants to help a child or grandchild pay for higher education or even K-12 private school. The flexibility to change beneficiaries or convert to ROTH IRA also prevents the funds being locked for education only. If you only use one strategy, the 529 provides the best tax savings and flexibility.

So now that we understand the existing options, let’s look at the new Trump account rules.

Pros - $1,000 Federal government seed money for a child born between 1/1/2025 and 12/31/2028. The entire balance will be converted to an IRA when the child turns 18. If managed through a practice Section 125 cafeteria plan, employees can contribute up to $2,500 in total to their children’s Trump account and receive a employer match of $2,500 (Note - this is optional for the practice, not required).

Cons - Total annual contribution limit of $5,000. Contributions provide no tax deduction. Total lifetime limit of $90,000 and investments are limited to US stock index funds. Withdrawals before 18 are taxable with early withdrawal penalty. On January 1st of the year the child turns 18, the account becomes an IRA and completely under their control. Any withdrawal or ROTH conversion from the account becomes a taxable event for the child.

Best For - Anybody with a child born in 2025 through 2028 to get the $1,000 government gift or high net worth family who has maxed out ROTH IRA and 529 contributions for their children.

Strategic Verdict for Your PRACTICE & Family Goals

For College Funding: The 529 plan remains the "landslide" winner. Because 529 withdrawals are 100% tax-free for education, this plan can save you 25–40% more than a Trump Account, which treats withdrawals as taxable income. The large lifetime limits and state contribution credits are also something not provided by the Trump accounts. Additionally, 529s are assessed more favorably (as a parent asset) for financial aid purposes compared to Trump accounts (a student asset).

For Retirement & Wealth Foundations: The ROTH IRA is superior. It offers a massive head start through 65 years of compound growth. By starting with the $7,500 and contributing the same annually until age 18, the ROTH IRA growing a 5% rate of return would create $2.2million in tax-free wealth for your child at age 65.

For New Parents in 2025-2028: The Trump Account is the only option that comes with a $1,000 government gift. You can stop there and your child would have $2,400 at age 18 (based on 5% return) or you could create a practice cafeteria plan that would allow you and your employees to contribute up to $5,000 annually tax free (total, not per child). With a 5% rate of return, your child would have a $143,000 IRA balance when they turned 18. Keep in mind that this balance upon withdrawal will be taxable.

Next Steps for Creating a Trump Account

For new parents wanting to access the Trump Account $1,000 Pilot Program, here is a coordinated approach.

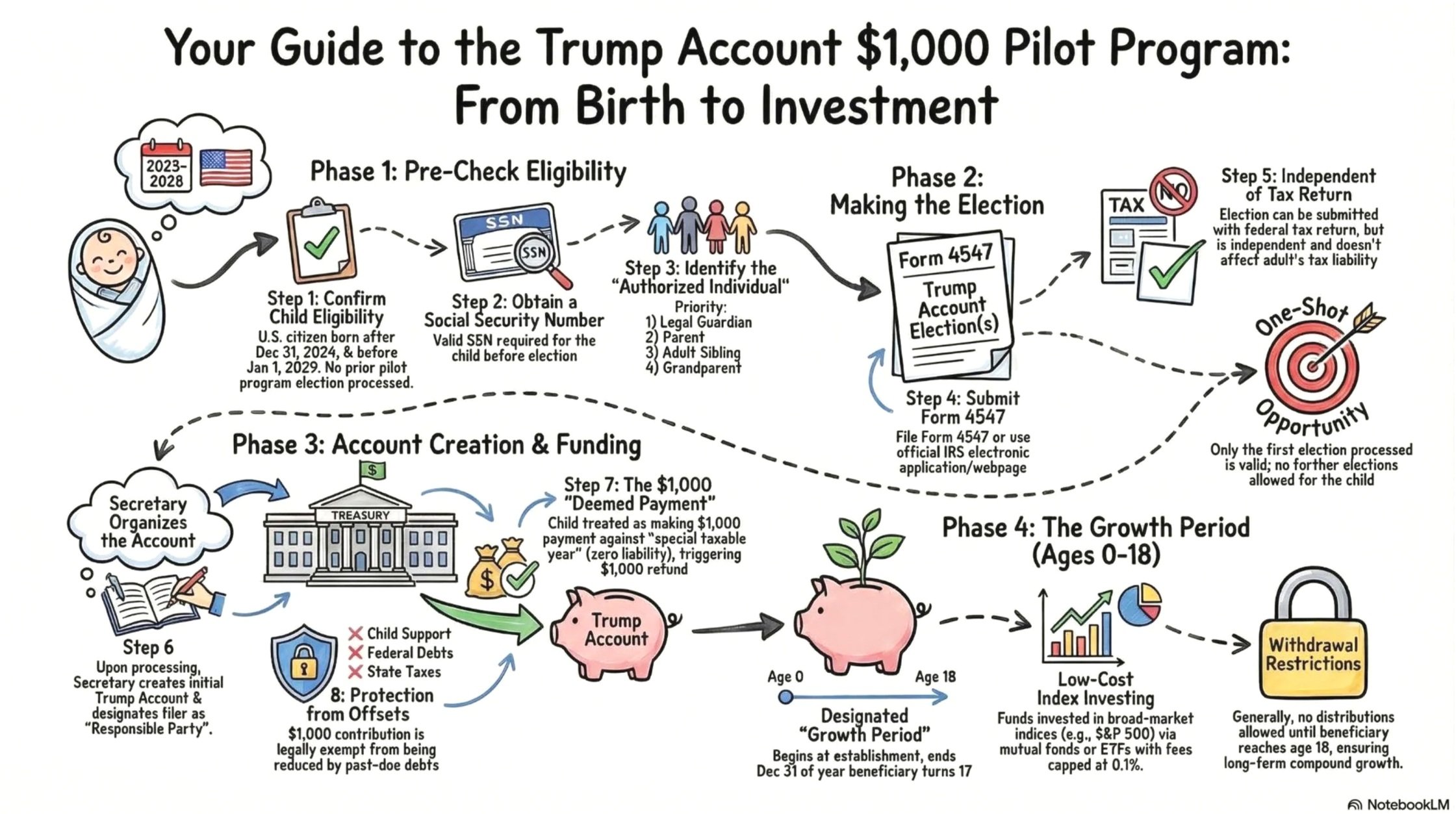

Determine Eligibility: Child must be US Citizen with a SSN number and born between 1/1/2025 and 12/31/2028. Only the authorized legal guardian can apply for the account.

Make the Election: The IRS has created Form 4547 to apply for the $1,000 seed money. You can file this form with your timely filed 2025 tax return or apply online here.

Account Creation and Funding: Once form is processed, the Department of Treasury will create an account and fund it when the program starts on July 4, 2026.

Growth Period: Decide whether you want to further fund the Trump account or focus on a ROTH IRA or 529 strategy for the next 18 years. But regardless of contributions, you should not withdraw these funds until they convert to an IRA in the year of the child’s 18th birthday.