Beware of the Personal Piggy Bank

Don’t Let Your Practice Become a "Personal Piggy Bank"

There are those times when you pull the wrong card out of your wallet at the store and pay a personal expense with your business credit card. The IRS is not going to send you to jail for those mistakes, especially if you treat it correctly as a shareholder distribution.

But intentionally paying personal expenses with your practice bank or credit card can get you in hot water with the IRS. Please refer to the cautionary tale of Hee v. Commissioner. In this case, a business owner treated his corporate treasury like a personal piggy bank, and the IRS eventually came back with a drill that went way deeper than a standard cavity.

Here are the top lessons every practice owner should take to heart:

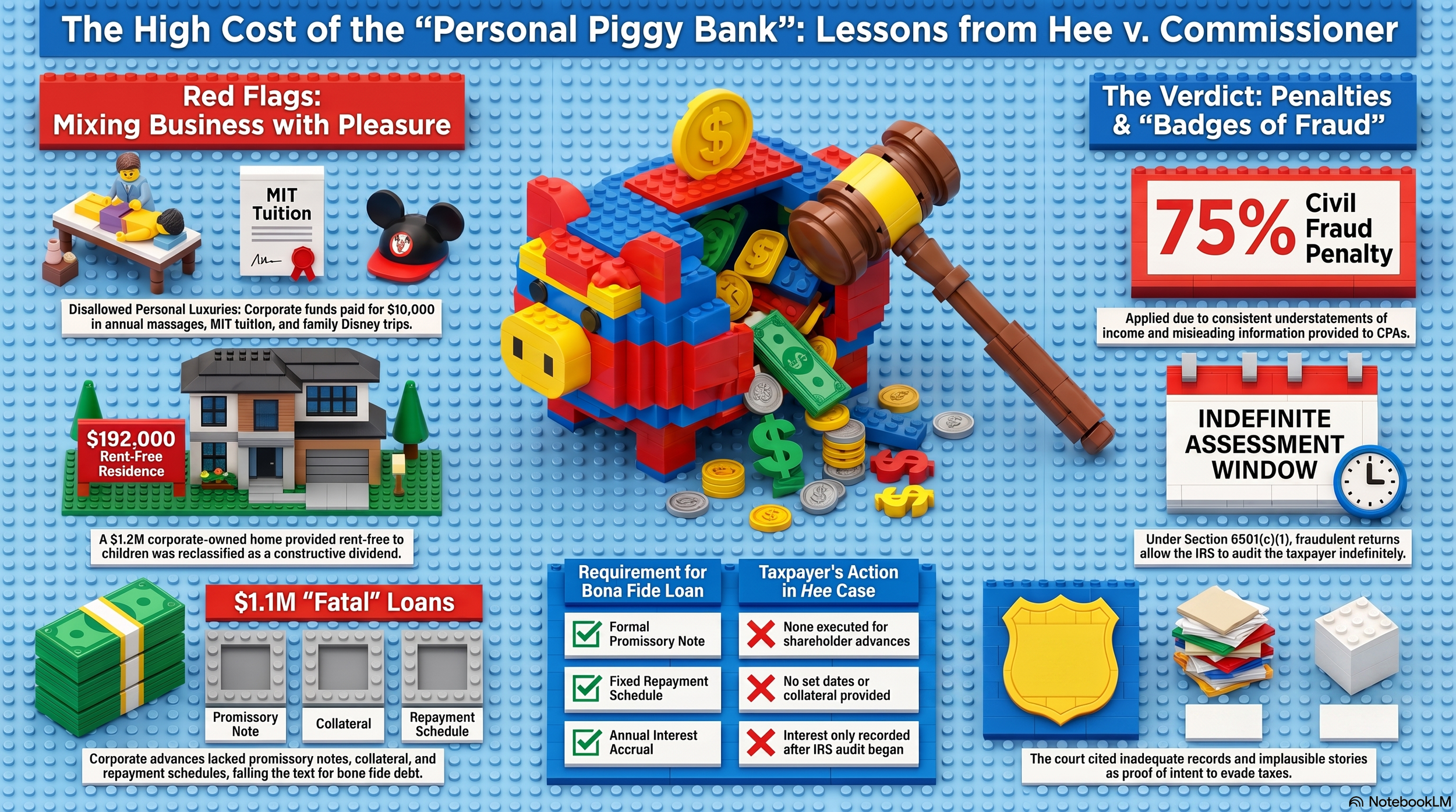

1. Massages and Mickey Mouse are NOT Business Expenses

We all need to de-stress, but Albert Hee took it to another level. He had his company pay for $6,000 to $10,000 annually in massages. He also billed the company for family trips to Disney World, Switzerland, Tahiti, and Kona. The Tax Court was not amused, noting that personal health and family vacations are "inherently personal costs" that don’t qualify as business expenses. If it’s not directly related to your dental practice, do not pay for it with practice funds. This includes not paying other business costs like your rental property costs with practice funds.

2. A "Loan" Needs More Than a Pinky Swear

Mr. Hee’s company advanced him over $1.1 million, which when challenged by the IRS, he claimed were "loans". However, there were no promissory notes, no collateral, and no repayment schedule. Because these "loans" lacked basic formalities, the IRS reclassified the entire balance as constructive dividends—meaning they became taxable income for him personally. If you’re borrowing from your practice, make sure you have a real contract and actually pay interest.

3. Family Payroll Isn't a "Gift"

It’s great to involve the family, but the Hee case shows the IRS has a "heightened scrutiny" for family compensation. Hee’s company paid undocumented salaries to his children and even paid $33,523 for his daughter’s MIT tuition, claiming it was an "educational" expense. Since there were no records of actual work performed and the daughter's education was way beyond the standard CE required at a dental practice, the deductions were summarily disallowed.

4. The 75% Penalty (The Real Root Canal)

This is where it gets scary. Because Mr. Hee consistently understated his income, kept inadequate records, and gave "implausible stories" to the IRS, he was hit with a 75% civil fraud penalty. Even worse, when fraud is involved, the standard three-year statute of limitations for audits is thrown out the window—the IRS can look back indefinitely. In fact, this specific case resulted in a criminal conviction for tax years dating back nearly 20 years before the 2026 decision.

The Bottom Line

Running a practice is hard work, and the tax perks can be great—if you follow the rules. Don't let your business become a "personal piggy bank". Keep your personal and business expenses strictly separate, document everything, and always listen to your CPA!